Here are the market thoughts and contingency planning ideas we recently shared with the advisory clients of Dennehy Weller & Co. We thought you might find them useful.

This current period has been called many things, The Age of Radical Uncertainty is one – though this is typically by those who think about and write on the markets rather than those in the markets. In contrast, for too many of those in the markets it is an age of extraordinary complacency.

For example, the US stock market has, on some criteria, never been more expensive including the Wall Street Crash, the bursting of the technology bubble, and the 2008 debacle.

Most big uptrends in markets have some sensible foundation. Then in its later stages it is taken too far. The stupidity of some people is combined with the greed of others, plus a sprinkling of fairy dust (debt) and then… crash.

The uptrend in Western markets and economies through the 1980s and 1990s was driven by the baby boomers (an “accident” of the Second World War), who reached their peak spending years. This was aided and abetted by easily available debt.

In contrast, progress in the years since the bursting of the tech bubble (the noughties and the teenies) has been largely driven by the actions of central bankers.

As we all know by now, their action was two-fold. Negligible interest rates and quantitative easing (QE).

Now the Federal Reserve is putting up interest rates and reversing QE (and other central banks are hinting at the same). They are doing so gradually for sure, but the foundations for the market recovery over the last 8 years are being withdrawn. That puts markets on a tight rope.

The positive demographic trend reversed around the millennium, but debt continued to pile up – the markets necessarily became increasingly vulnerable, culminating in the 2008 crash. In a similar way the foundation of the latest stock market upturn is being withdrawn.

Normally the stock market moves in lock-step with what we can call social mood – when there is greater confidence it will trend up, when there isn’t it will reverse – but these are not normal times.

That there has been a change in social mood is evidenced in election and referenda throughout the Western world. The trigger was the reversal in the positive demographic trend, combined with overwhelming debt which just kept growing. This didn’t suddenly happen in 2008, as some have suggested – the turning point was spread over years. Since that turning point economic dynamism and growth have been held back, and salaries have gone nowhere for many.

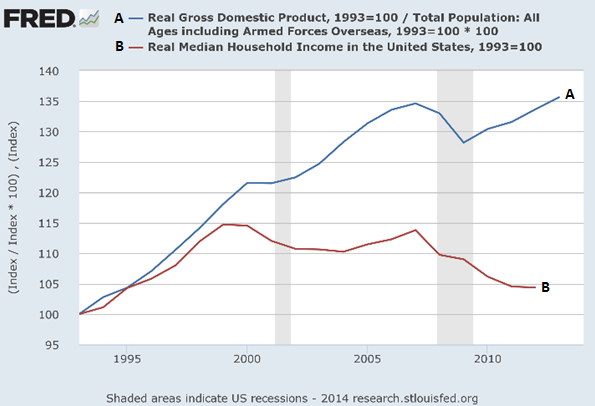

In the chart below you can see how household income in the US has stagnated and drifted lower since the late 1990’s - economic growth has continued edging up (though the economic recovery since 2008 is the weakest recovery ever recorded). This is mirrored throughout the West, where in many instances the US economy is the best of a bad lot.

The great unknown is when this social mood will be reflected in markets. The extraordinary intervention by central banks since 2008 has allowed markets to continue upwards. Even though that support is now being reversed, the timing of the market reaction to this is not known – there is no precedent for where we are today. We really would love to give you a clear answer – some formula to apply – a magic date. But there are none.

We have drawn the analogy with an avalanche-prone snowy slope, just waiting for the final snow flake - we don’t need to debate the shape or timing of the final snowflake - we just need to be prepared. The negative reaction is already happening socially and politically in the West - but markets are being artificially held up by central bank action, or at least have been to this point.

The good news is that in the last 30 years DWC have had a lot of experience of very sharp market downturns. Over those 30 years the market has ALWAYS given you a jolt to get your attention just before the worst. The sharpest falls in stock markets do not come from nowhere and without warning.

For example, after Lehman Brothers went bust you had a week or two to get out while “the smart money” was scratching its head. With “The Great Crash” in October 1987, which apparently came out of nowhere, the market had actually peaked in July, and even in the week prior to the Crash evidence mounted that it was time to sell – and we did.

The first sign that we are nearer the end should be a sharp-ish fall (perhaps 25%) which will trigger a tsunami of market obituaries as it unfolds. But this should merely be a dress rehearsal followed by a decent recovery - perhaps encouraged by the last trick up the sleeve of central bankers, helicopter money - more on that another time.

The latter picture is based on our experience. BUT there is no certainty. So we must also plan for being wrong! Humility is vital.

Beyond the worry-strewn Western world there is much to be encouraged by in Asia and some emerging markets. Demographics are mostly supportive. Japan is an obvious exception - but at least their stock market is cheap (relatively), and has a completely different (and more positive) social and political dynamic to the indebted west.

Asian stock markets as a whole cannot sidestep a downturn in Western markets - but they have bounce-ability, so should be bought on weakness.

Be prepared.

Part 2. The Contingency Plan

The scene was well and truly set in the last section. We must respond with a very clear plan for action.

Clear thinking is key. For example, there is no point having bits of this and bits of that to give a veneer of diversification.

Also, we don’t believe we should be in a fund just because we believe it will not fall as much as others – this is a bit woolly.

Plus, as we saw in 2008 with apparently lower risk corporate bonds, some funds can fall as much or more than those invested into stock markets.

Ideally, at this point the only funds we want clients to hold (in addition to cash) will be in one of two categories:

- A fund with clear growth potential, which you would be comfortable holding for years to come.

- A fund with clear potential do go up in the short term, in particular as stock markets and some bonds tumble.

That’s it.

The issues to address then become

- Which funds fall into category 1?

- Which funds fall into category 2?

- What % proportion should you have in cash now?

- How should this change as markets fall?

- How/when should you buy back in?

NEXT WEEK we will look at the above 5 issues in a blog for Gold Members. (Not a Gold Member yet? Do have a look here. Just £1 for the first month, how can you refuse?)

FURTHER READING