For years now, Growth investing has dominated headlines, powered by technology giants and ultra-low interest rates. Yet markets move in cycles and what has been out of favour often returns with strength. The Value investing style appears to be back in favour again.

The Case For Value Investing

Value investing rests on a simple idea. Buy strong companies at prices that do not fully reflect their long-term potential. These companies might be temporarily overlooked, facing near term headwinds, or simply be unfashionable. These situations create pricing gaps that patient investors can exploit.

Over long periods Value investing has delivered both downside protection and competitive returns. Value stocks tend to do well during economic recoveries and periods of economic uncertainty where investors place greater emphasis on current profitability and cash flows rather than distant earnings projections that drive many of the Growth stocks.

For more depth, exploration and the history of these trends see our earlier pieces on Why Value Matters and Value – A Sleeping Giant.

Growth vs Value: A Shifting Relationship

The interplay between Growth and Value evolves as conditions change. During the last decade Growth led markets, driven largely by US tech and AI businesses. Value often leads when the market broadens and investors focus on current profitability, strong balance sheets, and reliable dividends.

In 2025, the market narrative has flipped as demonstrated in Chart 1 below. After growth dominated in 2024, value has taken the lead, clearly outperforming growth as investors rotate toward cheaper, cash-flow-driven stocks.

Chart 1

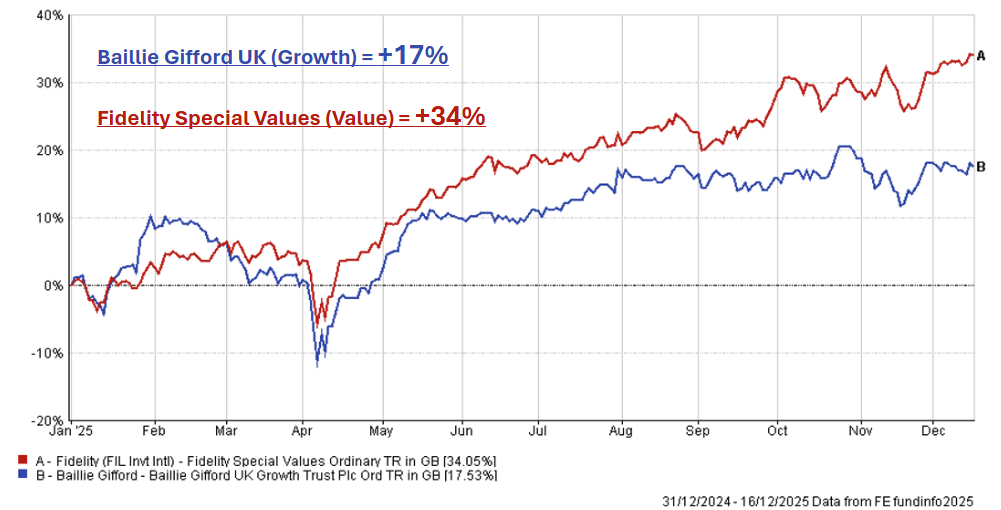

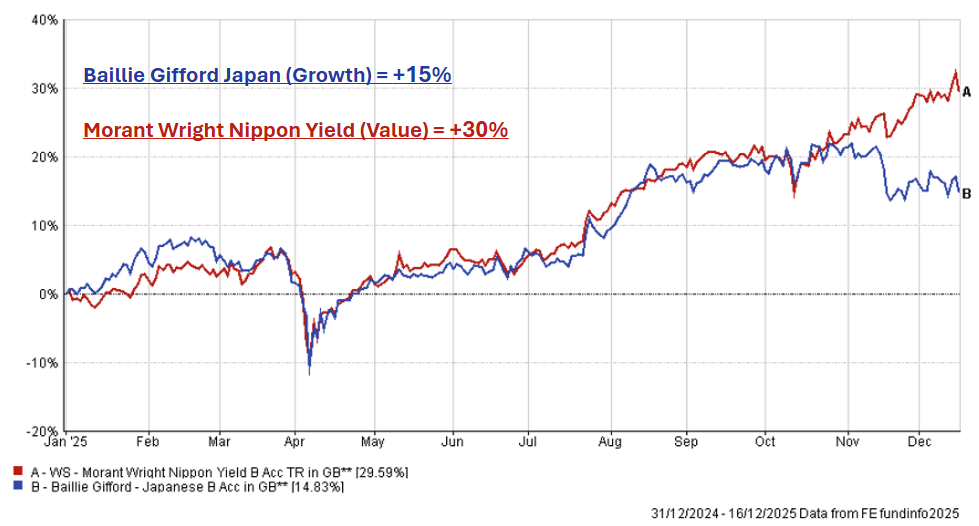

This leadership shift is also clear regionally, with Value outperforming Growth in both the UK (Chart 2) and Japan (Chart 3) during 2025 as investors increasingly favour cash generation, dividends, and balance sheet strength.

Top 20 Best Value Funds

Here our team have identified the 20 best-performing Value funds over 6 months across all sectors, and you can see that they are a very diversified group:

Name | Sector | 6 month performance (%) |

|---|

VT Price Value Portfolio | IA Flexible Investment | 43.34 |

JPM Korea Equity Fund | IA Specialist | 40.13 |

Nomura Japan Strategic Value ID Hedged | IA Japan | 32.02 |

Man Japan Core Alpha C Professional | IA Japan | 31.88 |

Barclays GlobalAccess Japan M Hedged | IA Japan | 31.1 |

NB US Small Cap Intrinsic Value | IA North American Smaller Companies | 30.9 |

M&G Japan | IA Japan | 30.29 |

Quilter Investors Japan Equity | IA Japan | 29.86 |

Heptagon Kopernik Global All Cap Equity | IA Global | 28.25 |

Artemis Global Income | IA Global Equity Income | 26.71 |

Fidelity Asian Special Situations | IA Asia Pacific Excluding Japan | 35.69 |

T. Rowe Price Emerging Markets Discovery Equity | IA Global Emerging Markets | 25.58 |

Artemis SmartGARP Global Emerging Markets Equity | IA Global Emerging Markets | 25.26 |

FundRock Management Company S.A. AMOVA Japan Value | IA Japan | 25.2 |

M&G Asian | IA Asia Pacific Excluding Japan | 24.08 |

Redwheel Global Intrinsic Value | IA Global | 23.98 |

M&G Global Emerging Markets | IA Global Emerging Markets | 23.97 |

FTGF Royce US Small Cap Opportunity | IA North American Smaller Companies | 23.9 |

BlackRock GF Japan Flexible Equity | IA Japan | 23.18 |

T. Rowe Price Global Value Equity | IA Global | 23.13 |

| | |

S&P 500 | | 11.20 |

FTSE 100 | | 14.96 |

Download our complete list of value funds, split by sector: Value Funds January 2026

Why This Matters for Investors

Value investing remains a powerful source of long-term returns. Periods of underperformance create attractive entry points and patience is often rewarded when the market rotates toward companies with strong cash flows and sensible valuations. It is also clear that, despite negativity around value in some quarters, buying funds with a value bias at the right time can pay off handsomely.

Timing is the hard part. Get in too early and the only consolation may be that a value fund falls less than other areas of the market. A practical approach is to use momentum indicators to identify when market sentiment is shifting towards value or growth funds. Nonetheless, the right value funds with strong underlying fundamental and a proven track record can outperform across different market environments.

Last but not least, in the weeks ahead we will look at why Value looks set to continue this outperformance versus the Growth style which had dominated for more than a decade.